Sweepstakes Casino Tax Guide: 1099-MISC, Thresholds and Filing Rules

Best Non GamStop Casino UK 2026

Loading...

Sweepstakes casino winnings are taxable income in the United States. That much is clear. What most players do not realize is that the tax treatment of SC redemptions differs significantly from traditional gambling winnings — starting with the form you receive and ending with what you can and cannot deduct.

Regulated casinos issue a W-2G for qualifying payouts. Sweepstakes casinos issue a 1099-MISC. That single difference in form type changes the reporting threshold, alters withholding rules, and eliminates the ability to offset winnings with losses in the way that traditional gamblers can. If you are redeeming Sweeps Coins for cash, understanding these mechanics is not optional — it is the difference between filing correctly and receiving an unexpected letter from the IRS.

This guide covers the tax rules as they apply in 2026, including a significant threshold change that took effect this year. It is not tax advice — consult a qualified professional for your specific situation — but it is the factual framework you need to make informed decisions about your SC redemptions.

Why SC Winnings Use 1099-MISC, Not W-2G

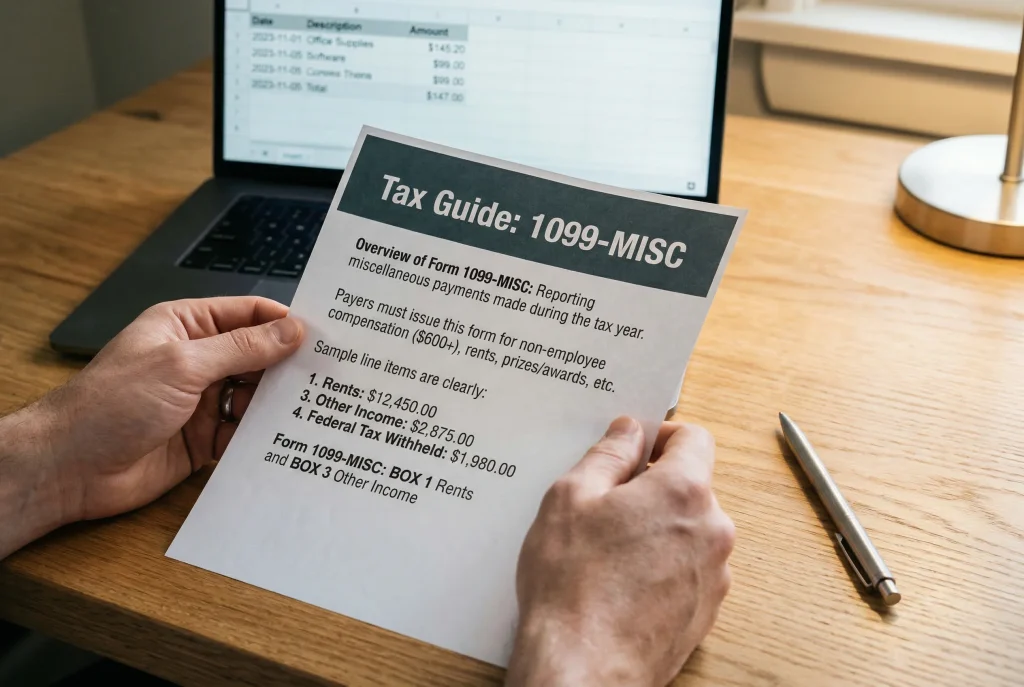

The tax form you receive depends on how the IRS classifies your income. Regulated casino winnings — from slot machines, poker tournaments, or table games — are classified as gambling income and reported on Form W-2G. Sweepstakes casino redemptions, however, are classified as prize income from a promotional sweepstakes, which gets reported on Form 1099-MISC.

This classification flows directly from the legal structure of sweepstakes casinos. Because operators are not licensed gambling providers and because Sweeps Coins are technically promotional prizes rather than gambling payouts, the IRS treats the income differently. Through 2026, sweepstakes casino operators were required to issue a 1099-MISC when a player’s total redemptions exceeded $600 in a calendar year. Starting in 2026, the One Big Beautiful Bill Act raised that threshold to $2,000 — a change that applies to both 1099-MISC and W-2G reporting.

The practical impact of receiving a 1099-MISC instead of a W-2G is substantial. On a W-2G, gambling winnings can be offset by documented gambling losses up to the amount of winnings, provided you itemize deductions on Schedule A. With a 1099-MISC, the income is reported as “other income” on Schedule 1, Line 8b of your federal tax return — and the offsetting rules are different.

Under the IRS gaming withholding and reporting threshold table, sweepstakes and lottery winnings have their own category with distinct reporting triggers. Prior to 2026, the $600 threshold for 1099-MISC reporting on sweepstakes prizes applied when the payout was at least 300 times the wager. Under the OBBBA, that reporting trigger has risen to $2,000 — though in the sweepstakes context, defining “the wager” remains legally ambiguous, since players may not have wagered any money at all.

For players crossing the $2,000 mark, the casino has your Social Security number on file and will report the total to the IRS. You will receive a copy of the 1099-MISC by January 31 of the following year. Whether or not you receive the form, the income is still taxable. The IRS expects you to report all income, including SC redemptions below the reporting threshold.

The distinction between 1099-MISC and W-2G also affects state tax treatment. Some states piggyback on federal gambling income rules for deduction purposes. If your state allows gambling loss deductions tied to W-2G income but has no equivalent provision for 1099-MISC prize income, you may face a higher effective tax rate on sweepstakes winnings than on traditional casino winnings — an ironic outcome given that sweepstakes casinos are often perceived as the more casual option.

Reporting Thresholds and Withholding Rates

The key numbers for sweepstakes casino players in 2026 are $2,000 and $5,000. The first is the new reporting threshold under the OBBBA — the point at which the casino must issue a 1099-MISC to you and the IRS. The second is the withholding threshold — above which the operator may be required to withhold 24% of the payout for federal taxes before sending you the remainder.

Here is how the thresholds work in practice. If you redeem a total of $1,500 in Sweeps Coins during 2026, no 1099-MISC is triggered because the amount is below the new $2,000 threshold. You are still responsible for paying the applicable federal and state income tax when you file your return — the IRS expects all income to be reported regardless of whether a form is issued. The tax rate depends on your overall income and filing status.

If your annual redemptions exceed $5,000, the casino may withhold 24% at the source. On a $6,000 redemption, that means $1,440 withheld and $4,560 paid to you. The withheld amount is credited against your total tax liability when you file. If your effective tax rate is lower than 24%, you will receive a refund of the difference. If higher, you will owe additional tax.

There is an important nuance: the $2,000 threshold applies to total annual redemptions, not to individual transactions. A player who redeems $700 three times throughout the year has crossed the threshold, even though no single redemption was large. The casino tracks cumulative totals and triggers reporting accordingly. Note that some states may not adopt the higher federal threshold — check your state’s specific requirements.

For players reporting SC income, the line item is Schedule 1, Line 8b (“Other Income”) on the federal 1040 form. This is the same line used for jury duty pay, hobby income, and other miscellaneous sources. It does not carry the same deduction privileges as gambling income reported on Schedule A.

The 2026 Threshold Change: What It Means

Starting with tax year 2026, the reporting threshold for slot machine winnings has increased from $1,200 to $2,000 under the One Big Beautiful Bill Act. The threshold will also be indexed to inflation going forward, meaning future adjustments will happen automatically rather than requiring new legislation. This is the first increase since the $1,200 figure was set in 1977.

For sweepstakes casino players, the impact is broader than the W-2G change alone. The OBBBA also raised the 1099-MISC reporting threshold from $600 to $2,000 for payments made starting in 2026, with inflation indexing beginning in 2027. This means sweepstakes casinos are no longer required to issue a 1099-MISC until a player’s cumulative annual redemptions reach $2,000 — up from $600 previously. A player who redeems $1,500 in SC during 2026 will not trigger a 1099-MISC filing, whereas the same redemption in 2026 would have. The change, confirmed by legal analysis from Frankfurt Kurnit Klein & Selz, applies to all promotional sweepstakes prizes — including SC redemptions. However, the income remains taxable regardless of whether a form is issued. The IRS still expects you to report all prize income on your return.

Jeff Duncan, former US Congressman and Executive Director of the Social Gaming Leadership Alliance, addressed the regulatory posture of the sweepstakes industry at the NCLGS Conference in December 2026. His position: the industry actively seeks formal regulation and taxation rather than operating in a legal gray area. That stance — whether taken at face value or not — signals an awareness that the current tax framework may evolve as legislators pay more attention to the sweepstakes model.

An additional OBBBA change that affects all gamblers: starting in 2026, the deduction for gambling losses is capped at 90% of documented losses, rather than 100% as previously allowed. This means a player with $10,000 in winnings and $10,000 in documented losses can now deduct only $9,000, creating $1,000 of taxable “phantom income.” While this primarily impacts players at regulated casinos who report on W-2G, it further underscores the evolving tax landscape around gaming in the US.

For now, players should plan around the new $2,000 reporting threshold for 2026 and ensure their tax preparation accounts for 1099-MISC income from SC redemptions. The rules are shifting — but the obligation to report all income does not.

Can You Deduct Gold Coin Purchases as Losses?

The short answer is no. And the longer answer explains why.

When you buy a Gold Coin package at a sweepstakes casino, you are purchasing a virtual entertainment product — not placing a bet. The IRS allows gambling loss deductions (up to the amount of gambling winnings) for activities that qualify as gambling under tax law. Since sweepstakes casinos are structured as promotional sweepstakes and not licensed gambling operations, your Gold Coin purchases do not meet the definition of a gambling wager.

This creates an asymmetric tax position. Your SC redemptions are taxable income. Your GC purchases are not deductible losses. If you spend $500 on Gold Coin packages over the course of a year and redeem $800 in Sweeps Coins, you owe income tax on the full $800 — not on the $300 net difference. This is fundamentally different from how a regulated casino player would be treated, where the $500 in losses could offset the $800 in winnings if the player itemizes deductions.

Some players have explored whether GC purchases could be classified as a hobby expense or a cost of generating prize income. The IRS is generally skeptical of such arguments, and no established precedent supports deducting sweepstakes casino purchases as a business or hobby expense. Unless and until the tax code or case law changes, Gold Coin purchases should be treated as non-deductible personal entertainment spending.

The practical takeaway: keep records of both your purchases and your redemptions, even though only the redemptions are currently relevant for tax purposes. Tax treatment of sweepstakes casinos is still evolving, and having clean documentation protects you regardless of how the rules develop. If your total annual redemptions stay below $2,000, you will not receive a 1099-MISC — but you are still legally required to report the income on your return.